Sometimes when they leave the nest, they find their way back again…but what kind of impact does continuing to support your adult children have on your retirement security?

Sharing a report from NerdWallet below, which says that future retirees lose about $227,000 in possible retirement savings from helping their adult children pay for their groceries, rent or housing and other bills. It’s an eye-opening number: while some of these expenses might seem small on a monthly basis, in reality they add up over time. Bottom line: parents may not be realizing the degree to which this affects their retirement.

————————————————————–

By Erin El Issa

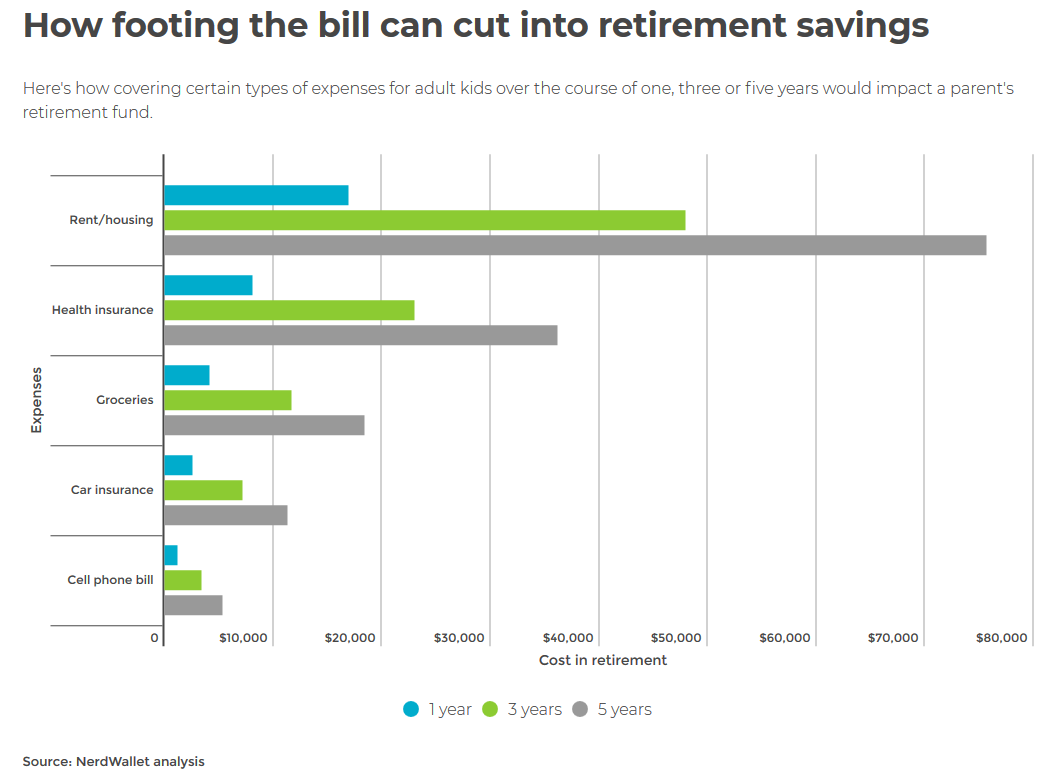

Many parents of children 18 and older are paying or have paid for their adult children’s basic living costs, including groceries (56%), health insurance (40%) and rent or housing outside the family home (21%). Some parents are also covering or have covered their adult child’s cell phone bill (39%) and car insurance (34%). But it’s important for parents — especially those who are behind in saving for retirement — to note that those same dollars could significantly grow their nest eggs over time.

More than a quarter of parents of children 18 and older (28%) are paying or have paid for tuition or student loans for their adult child. Considering the average parent borrows $21,000 for their child’s tuition and student loan payoff plans are around 10 years, it’s potentially costing these parents almost $80,000 in retirement savings to send their kid to college. This doesn’t include any money parents saved for their child’s tuition, which if prioritized over retirement could push this savings loss even higher.

On average, a parent covering a child’s living expenses for five years and borrowing money for college tuition is missing out on $227,000 — almost a quarter of a million dollars — in retirement savings. A higher cost of living or supporting multiple adult children could drive that number even higher.

In addition to these living costs, some parents of children 18 and older are paying or have paid for other expenses, such as clothing (32%), entertainment (20%), an allowance (10%) or a car loan (10%).

We didn’t include these expenses in the total hit to retirement savings in our analysis, but any amount a parent gives their adult child that they could otherwise save might be derailing their retirement plans. Suppose a parent gives an adult child an allowance of $200 a month for five years. That $12,000, invested in a retirement account earning 6% interest, would grow to almost $40,000 by the time the parent retires.

Over half of parents of children of any age (57%) say they’re confident that they’re contributing enough to their retirement savings, and if that’s the case for you, helping your children financially may not hurt you. However, if this help comes at the expense of your own retirement savings, it can significantly impact your standard of living later in life.

Parents tend to want to do everything they can to help children succeed. But sometimes they focus on the present at the expense of the future. Rather than taking money from your own savings and putting your retirement security at risk, look for ways to help your children that are good for your finances and theirs.

For example, keeping your kids on the family insurance plan as long as possible might help your child save on health care costs. But ask your children to reimburse you for at least some of those costs, and maybe ramp up the amount they contribute over time. That’ll help get them ready to pay their own bills down the road, even as it keeps you on track to save for retirement — which is when you’re really going to need that money.

When it comes to student loans, if you’ve already taken out parent PLUS loans for your child, you can ask them to contribute to the bill. You can also refinance your loans or speed up repayment to reduce interest charges.

If you haven’t yet taken out loans for your child but plan to, it’s a good idea to have your child borrow first. Federal student loans tend to have lower interest rates than parent PLUS loans, and your child will have plenty of time to pay them before retirement. You can still help if it won’t hurt your own savings.