The Tax Cuts and Jobs Act (TCJA) includes many changes that will affect individual taxpayers for 2018-2025. However it maintains the status quo for taxes on long-term capital gains (LTCGs) and qualified dividends. But the way it did so was confusing. Here’s what you need to know to dispel any confusion.

Rates and brackets for LTCGs and dividends before the TCJA

Before the TCJA, you faced three federal income tax rates on LTCGs and qualified dividends: 0%, 15%, and 20%. Those rate brackets were tied to the ordinary income rate brackets:

- If the LTCGs and/or dividends fell within the 10% or 15% ordinary income brackets, your tax rate was an unbeatably low 0%.

- If they fell within the 25%, 28%, 33%, or 35% ordinary income brackets, your tax rate was 15%.

- If they fell within the maximum 39.6% ordinary income bracket, you paid the maximum 20% rate.

Of course higher-income folks were also exposed to the dreaded 3.8% net investment income tax (NIIT). So many actually paid 18.8% (15% + 3.8% for the NIIT) or 23.8% (20% + 3.8%) on LTCGs and dividends instead of the advertised 15% or 20%.

Rates and brackets for LTCGs and dividends after the TCJA

The TCJA retains the 0%, 15%, and 20% rates on LTCGs and qualified dividends. However for 2018-2025, these rates have their own brackets that are no longer tied to the ordinary income brackets. Here are the 2018 brackets for LTCGs and dividends.

After 2018, these brackets will be indexed for inflation.

Higher-income folks are still exposed to the 3.8% NIIT. So if you are in that category, you could still owe 18.8% (15% + 3.8% for the NIIT) or 23.8% (20% + 3.8%) to the Feds instead of the advertised 15% or 20%.

TCJA rates and brackets for LTCGs and dividends collected by trusts, estates, and kiddie tax victims

Just so you know, here are the 2018 rate brackets for LTCGs and qualified dividends collected by trusts and estates.

- 0% tax bracket: $0-2,600

- Beginning of 15% bracket: $2,601

- Beginning of 20% bracket: $12,701

For 2018-2025, the TCJA stipulates that these trust and estate rates and brackets are also used to calculate the dreaded Kiddie Tax when it applies to LTCGs and qualified dividends collected by dependent children and young adults. The Kiddie tax can potentially apply until the year during which a dependent young adult turns age 24 if he or she is a student. Under prior law, the Kiddie Tax was calculated using the marginal rates paid by the parents.

There you have it: the scoop on how LTCGs and qualified dividends are taxed under the new law.

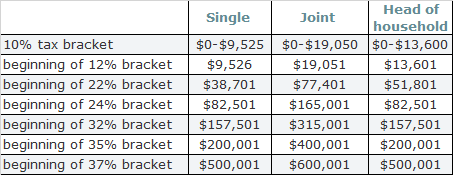

2018 Tax rates and brackets for short-term capital gains

As under prior law, the TCJA taxes short-term capital gains recognized by individual taxpayers at the regular ordinary income rates. For 2018, the ordinary income rates and brackets are as follows.