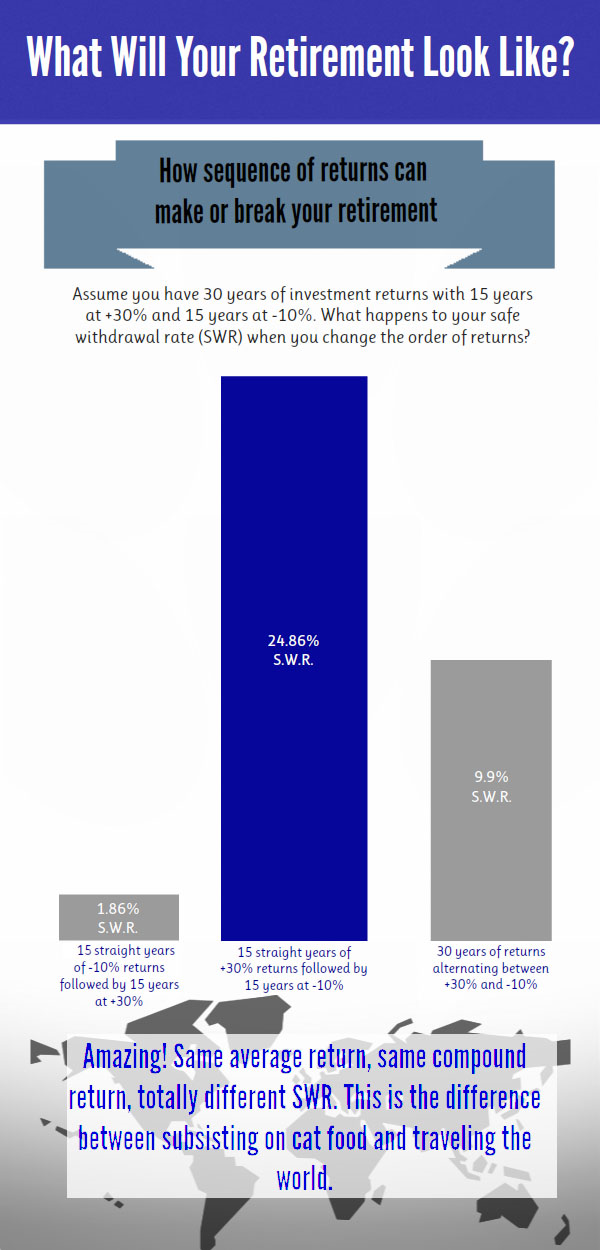

The current U.S financial market environment is anything but average – we’re at a point in the cycle where the stock market’s value is relatively high when comparing historical P.E. ratios, and interest rates on “safe” investments like government bonds continue to be kept historically low. To give you a taste of how future returns can really play with an assumed safe withdrawal rate, here’s a simple graphic to illustrate. In each scenario you have the same time horizon, same average return over that time horizon (10%), and an equal number of years of 10% losses and 30% gains over the time period. The only difference between each scenario is the sequence over which you experience those losses.

In example 1, your time horizon is front loaded with 15 straight years of 10% losses, followed by 15 years of 30% gains. If you were unlucky enough to retire to such a scenario, you’d only be able to sustain a 1.9% safe withdrawal rate.

Example 2 is a brighter side view; this time you experience just the opposite and your early years are all positive. Here your safe withdrawal rate over 30 years is a whopping 24.9%!

Example 3 alternates gain and loss years and comes up with a 10% safe withdrawal rate.

A couple of key points jump out at me when it comes to sequence of returns as demonstrated here:

- The early years of retirement and their performance are really important when it comes to your portfolio’s ability to generate retirement income

- Even though your portfolio achieves an average return over time, how it gets there can really effect how much you can safely take out

So for us, while we understand the allure of something like the 4% rule as a simple solution for figuring out how much income to withdraw from your investment portfolio, it should not be seen as the answer when it comes to retirement planning. The next logical question is what’s the alternative?

Planning and Flexibility

It’s our belief that having a plan that continuously checks your progress and a willingness to be flexible when it comes to the income you draw from your assets are paramount to a successful retirement.

How Having a Plan Helps

Rather than base how much you pull from your portfolio on a flawed rule of thumb, we strongly feel it pays to run through actual retirement plan scenarios, especially as you are entering retirement, in order to feel comfortable with the amount of income you can afford to take from your savings.

- Running the numbers provides a starting point

- Continuous annual reviews and recalculations of withdrawals (up or down if necessary) keeps plan on track

- Plan stays based on “real-time” numbers – for expenses, portfolio values and returns so you are more easily able to discern when adjustments are necessary

Flexible spending opens up many possibilities

Remember In real life we adjust our spending based on the success or failure of our careers and the income they produce. Why should retirement be any different?

Your retirement plan is your guidebook through retirement; it sets the baseline and gives you something to track your performance against. It also gives you a heads up when adjustments need to be made so that you don’t run out of money before your time. And being open to the idea of flexible spending makes the adjustments easier to make.