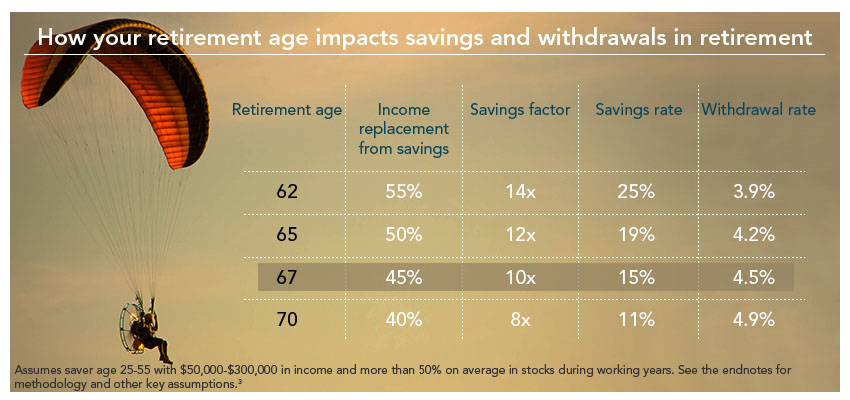

In another tidbit from Fidelity’s Retirement Savings Assessment study, the firm took a look at the impact your retirement age has on the appropriate annual savings and withdrawal rates. See their findings below:

An early retirement would mean that you have less time to save and a longer retirement to fund. The average age for retirement is 62, which is an important factor because that is when you can start claiming Social Security benefits. However, waiting to claim Social Security until age 70 could substantially increase your monthly benefits. So the age at which you choose to stop working has a big impact on how much income you need from your own savings. This, in turn, affects other rules of thumb like savings rate, savings factors, and sustainable withdrawal rates.

While you may not be able to pinpoint exactly how much income you may need in retirement, you probably have an idea about when you want to retire. If you’re planning to retire early, you may want to use the rules of thumb for age 62. If you are planning to work longer, the rules for age 70 might be more appropriate for you.

We devised a series of guidelines that take into account the important role of retirement age and Social Security. See the following table for a quick summary of how retirement age impacts the other guidelines.

3. The savings factor, savings rate, and withdrawal rate targets are based on simulations based on historical market data. These simulations take into account the volatility that a variety of asset allocations might experience under different market conditions. Given the above assumptions for retirement age, planning age, wage growth, and income replacement targets, the results were successful in nine out of 10 hypothetical market conditions where the average equity allocation over the investment horizon was more than 50% for the hypothetical portfolio. Remember, past performance is no guarantee of future results. Performance returns for actual investments will generally be reduced by fees or expenses not reflected in these hypothetical calculations. Returns will also generally be reduced by taxes.